Market update - November 2020

Market Update September 2020

The world has been living with the COVID 19 virus for most of 2020, and as we learn to live with lockdowns and the prospect of a vaccine draws closer, our thoughts are turning to what the world will look like Post COVID, and what changes should investors consider making now to position for the Post COVID world.

Some sectors such as Tech stocks and online retail have benefited from the virus, and this has been priced into their share prices. Many investors are asking the question: is now a good time to buy stocks? Some sectors such as hospitality, in store retail and banking have been negatively impacted by the virus and their share prices have correspondingly dropped. In this document we address the banks, property, gold and low interest rates.

Banks

The COVID lockdown has led to significant earnings reduction by the banks, and this flows on to reduced dividends. CBA profit down 11% earnings, dividend down 30%, ANZ and NAB dividends down 70%, and WBC no dividend.

In March 2020 when lockdown started, and thousands of Australians were losing their jobs, the banks allowed those affected to pause their mortgage payments for 6 months. The interest on these loans still accrues - it is just added to the loan - so on paper the banks are still profiting from the interest, however they are not receiving the cash from mortgage repayments so don’t have the cash to pay dividends

Govt stimulus also kicked in in March and started winding down in September. We expect that the government will retain some level of stimulus going forward to ease the transition process for individuals and businesses post lockdown.

The government stimulus and pause on loan repayments prevented many ordinary Australians from facing a cashflow crisis, however when these measures wind down, the underlying problem will still be there. When the stimulus measures were announced, the time frame of dealing with the virus was a big unknown so 6 months was chosen. 6 months down the road, the government partially extended the stimulus measures, and lenders can approach their bank to help ease back into repayments whether that be interest only loans, or a further extension of the pause on loan repayments. The banks and the government are likely to extend the stimulus and support measures until lock down is no longer required and the economy can return to some level or normalcy. Regardless of the timing, the stimulus measures have started winding down and this will place further pressure on banks’ profits in the coming months

Aside from the issues caused by the COVID lockdown, banks were already facing pressures from increased regulation due to the findings of the banking royal commission. One of the key take-outs from the royal commission was the greater emphasis on responsible lending obligations. This placed the ultimately responsibility on deciding whether a borrower can afford to pay a loan onto the banks. Since then, it has become increasingly more difficult to obtain credit as anyone who has applied for credit recently will tell you. The government argues that the pendulum has swing too far and that the borrower should take on some of the responsibility to determine if they can afford a loan or not. If these proposed changes come through, then it will make obtaining credit easier, which would then flow through to the economy.

Other issues that the banks are facing:

- Credit growth slow due to borrowers not wanting to borrow

- Net Interest rate margins are falling due to competition which means the banks aren’t making as much on their loans.

- The financial shock that consumers have felt due to lockdown has led a change from credit to debit cards which means fees fall as well as lower activity.

- Staff are not taking leave because they cannot travel and many are working from home, so annual leave entitlements are accumulating which the banks need to make an allowance for.

The issues facing the banks are mostly driven by COVID lockdowns. The recovery from this will hinge on when lockdowns end and there are three possible scenarios for the recovery.

The first is a V shaped recovery meaning that the economy bounces back as quickly as it dropped. The longer the lockdowns continue, the less likely this is to occur. The second and most likely is a U shaped recovery where the recession caused by the lockdowns takes a longer period of time to end. The third scenario is a drawn out recovery where it takes a decade or longer to recover. Given the amount of government stimulus and the ‘whatever it takes’ approach of central banks around the world, we believe this scenario is unlikely.

If a V shaped recovery occurs, then now would be the time to buy banks however if the likely scenario of a U shaped recovery occurs then it would be prudent to hold off buying or adding to bank stocks for now.

Given the banks are the beating heart of the economy, they perform better in a stronger economic environment, so when the signs of economic recovery start appearing, the banks will be an attractive investment.

Fixed interest – Term deposits, Cash and Bonds.

The Reserve Bank of Australia reduced interest rates to a historic 0.1% in November, and rates are expected to stay low for several years. The reserve bank in their statement that accompanied November’s meeting said that they are “not expecting to increase the cash rate for at least three years”. The US have made similar statements with the Federal Reserve saying they are not “thinking about, thinking about, thinking about raising rates”. That’s not a typo, he said it three times to emphasis the point that rates will be low for a long time. The result is that short term rates are nailed to the floor and interest from cash and term deposits will likely stay very low for several years to come.

In addition to low interest rates, there is an avalanche of supply of money being introduced into the system by governments in their efforts to counter the COVID lockdowns. Extra supply means that bond prices reduce, and yield increases.

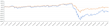

As a result we are seeing the yield curve steepen. The yield curve is simply a plot of interest rates of different durations. A steepening of the yield curve means that long term rates are higher than short term rates, and typically indicates economic optimism. With short term rates nailed to the floor, the long end of the curve is the only thing that can reflect the markets expectations regarding inflation and economic growth.

The graph shows that compared to 6 months ago, the US yield curve has steepened. This means that longer term rates are higher than short term rates and is a good sign that economic recovery is expected, however it also means that cash and term deposit interest rates are at historic lows.

All this bodes poorly for cash and term deposit money. Cash and Term Deposits are an important part of a portfolio as they provide liquidity and stability, however their ability to deliver income in the coming years is expected to be poor. We have added the Ardea Real Outcome Fund, and Gold to the portfolio to help mitigate the low cash interest rates.

Gold

With low interest rates and the expectation that inflation will increase due to massive government stimulus, Gold becomes an attractive investment option. Gold traditionally is a volatile asset, and given it doesn’t pay interest, it doesn’t suit the requirements of many investors however can have a positive effect on a diversified portfolio

Gold is an asset that many investors flee to when economic uncertainty hits, and this has certainly been the case in 2020. The Gold price is up 25% since January and we expect the upside pressure on the price to continue.

In a research paper on Gold as an investment, Morningstar had this to say on adding gold to a diversified portfolio:

“Looking at risk and return trends over the past 15 years, the argument for adding gold to a portfolio looks pretty convincing. Portfolios with heavier gold weightings had lower volatility and higher Sharpe ratios.”

We are adding a modest allocation of GOLD to our portfolios through the ETF called Physical Gold with ASX code GOLD.

Property

Australian Listed Property

Australian listed property was among the best-performing asset classes of the third quarter of 2020, finishing up 7.0% however is still down 20% year to date. Renewed optimism around a relaxation of social distancing measures flowed through into better sentiment toward this asset class. Nonetheless, COVID-19 has acutely affected this asset class, appearing to accelerate the trend toward online shopping (at the expense of foot traffic through shopping malls), while questions remain regarding the outlook for demand for office space, given the shift toward ‘working from home’. This has seen significant divergence in the performance of individual companies, with many enacting dividend cuts and capital raisings in order to help weather this period of extreme uncertainty.

At the start of 2020 we held underweight positions in listed property because we held the view that the sector was expensive. Due to the uncertainty surrounding the long term impact of COVID-19 on this sector, we are further reducing exposure to listed property in our model portfolios.

Residential Property

Residential Property in Australia has been remarkably resilient during 2020 given the severity of the impact COVID-19 had on peoples lives. Looking back at the last recession Australia experiences in the early 90’s property prices dropped dramatically and took a number of years to recover. This time the impact has been softened by government stimulus and the banks pausing mortgage repayments for those affected by COVID lockdowns.

Interest rates are also at historical levels which further supports property owners with mortgages.

Rents have been reducing on the back of higher supply as short term rentals like Air BNB are moved into the long term market, and demand has reduced as younger renters who have lost their jobs due to COVID move back in with their Parents.

Moving forward we expect residential property to continue benefit from record low interest rates, however if the economy worsens and takes longer than expected to recover, there could be further downside to Property prices.

Diversified approach

One strategy that has been confirmed during the recent volatility is that diversification works. A diversified portfolio has a mix of different asset classes such as property, shares, cash and fixed interest and holding an appropriate mix of each of these assets has a smoothing effect on returns. The following graph is an actual example of a typical ‘Balanced’ portfolio (orange line) last financial year, in comparison to the Australian stock market (blue line)

From this graph, we can see that between July 2019 and February 2020 when the market was performing well, the balanced portfolio participated in the upside, however when the market dropped significantly in February, the balanced portfolio didn’t drop as quickly and has benefited from the recovery.

Sticking to a balanced portfolio is a proven strategy and forms the basis of our recommendations to you.

Changes to portfolios:

Add GOLD – 2%

Add Ardea – 5%

Reduce SLF – reduce by 2%

Reduce Term Deposits – reduce by 5%

Ardea Real Ourcome Fund (XARO)

Ardea’s unique investment approach combines the safety of investing in high quality government bonds with proven risk management strategies that protect your capital from interest rate fluctuations and general market volatility.

This Fund is designed for those seeking:

• a higher expected return than cash

• an alternative source of income, with low volatility

• a defensive fixed income anchor to diversify portfolio risk away from equities, property and credit investments

• investors who accept some risk that their investment will include some exposure to derivative strategies and capital loss

The Fund has a track record of delivering returns exceeding cash and inflation since inception . As these returns are independent of market direction, Ardea expect to maintain a level of outperformance in rising and falling markets irrespective of the level of the cash rate.

The Fund offers daily liquidity, without break costs that can apply to certain cash products.

The Fund includes investments in high-quality government bonds and cash securities, which have lower credit risk, unlike bank hybrids and corporate bonds, while also using sophisticated risk management strategies to help minimise volatility compared to dividend paying stocks.

In addition to outperforming cash, the Fund targets returns exceeding inflation, which helps protect the long term purchasing power of your investment.

Unlike traditional fixed income funds, which may suffer from poor returns when interest rates are low, and may also incur capital losses if rates rise, the Fund does a lot more than just buy bonds to earn interest income. The Fund adopts a ‘relative value’ investment strategy to access a much broader range of fixed income return sources that are independent of the level or direction of interest rates. Investors can achieve better investment outcomes because the Fund can deliver stable returns that are independent of the broader fixed income and equity market fluctuations that may impact conventional funds. Additionally, in Australia the most popular income seeking investments – dividend paying stocks, bank hybrids, investment properties and credit funds – can become closely linked to each other in periods of economic stress, potentially incurring losses at the same time.

The Fund provides an alternative source of income that can deliver positive returns at these times, because its return sources are unrelated to conventional investment strategies. The Fund also includes sophisticated risk management strategies that are specifically designed to profit in volatile markets. So, in addition to providing stable income, the Fund can act as a defensive fixed income anchor to diversify your portfolio risks and help stablilise your investments against adverse market movements. A final unique benefit comes from the Fund’s return target being measured against the Australian Consumer Price Index (a measure of inflation). This means it targets returns not just exceeding cash but also exceeding inflation to help protect the long term purchasing power of your capital.

Morningstar’s take on Ardea:

Ardea Real Outcome is an attractive offering due to its seasoned team and well-structured risk-aware process. The strategy targets stable returns of 2% above inflation with low volatility over the medium term. The team skilfully applies a relative value approach, in which they have significant expertise. The strategy's universe is comprised of high-quality government bonds from countries with high (AA-AAA) credit ratings, inflation linked bonds, interest rate derivatives and cash securities. We like the smart combination of quantitative methods and qualitative judgment applied in identifying true mispricing opportunities. After selecting the trades, the team isolates interest rate duration using derivatives and constructs the final portfolio. The team targets and ably delivers little correlation to broader fixed income markets. Its relative value approach means performance will differ from the typical manager. Risk management is top of mind for Ardea. Each trade is scrutinised and sized according to its risk contribution to overall portfolio volatility (targeted at 2%). The portfolio includes risk-on and risk-off positions to deliver outperformance in various market environments. The final book is geographically diversified with 300-400 modestly sized trades. The portfolio is monitored and stress-tested to ensure the optimal balance between trades and their sizing. Ardea has developed strong infrastructure to accommodate the needs of this high-touch strategy. The team boasts extensive experience and stability with no departures to date. Five portfolio managers and the chief investment officer are jointly responsible for the portfolio, mitigating key person risk. The broader team includes three dealers, a risk analyst and a head of research. Positively, Ardea has boosted its resources in response to growing FUM. The strategy has performed strongly delivering on both its return and risk objectives since inception. A competitive fee adds appeal. Overall, we are confident Ardea's Real Outcome team of experts and their sound, well-considered investment process, will serve investors well.

GOLD

ETFS Physical Gold (GOLD) is designed to offer investors a simple, cost-efficient and secure way to access physical gold by providing a return equivalent to the movements in the gold spot price less the applicable management fee. GOLD is backed by physical allocated gold and each share represents a beneficial interest in approximately 1/10th of one fine troy ounce of physical gold held by JP Morgan Chase Bank, N.A., the Custodian Bank, in vaults in London. The management fee is 0.4% p.a.

General Advice Disclaimer: The information in this report is general advice only and does not take into account the financial circumstances, needs and objectives of any particular investor. Before acting on the general advice contained in this report, an investor should assess their own circumstances or seek advice from a financial adviser. Where applicable, the investor should obtain and consider a copy of the prospectus or other disclosure material relevant to the financial product before making any investment decision to acquire a financial product. It is important to note that the price or value of financial products go up and down and past performance is not an indicator of future performance.